Reinsurance premium rates increased. Interest rates remained high

0 comments

In 2024, reinsurance premium rates increased, interest rates remained high, and capital markets performed well. The composite achieved its highest ROE in five years. Retained earnings grew due to strong underwriting and solid net investment income. Surplus rose, driven by unrealized capital gains, lower dividends, and reduced share buybacks. This improved balance sheets across the industry, according to Beinsure Media analysis Global Reinsurance Market Trends.

The Best’s Special Report, notes that composite of reinsurers’ gross premiums written represented almost 90% of total reinsurance industry gross premium written in 2022 and includes companies reporting using U.S. GAAP and IFRS 17 standards.

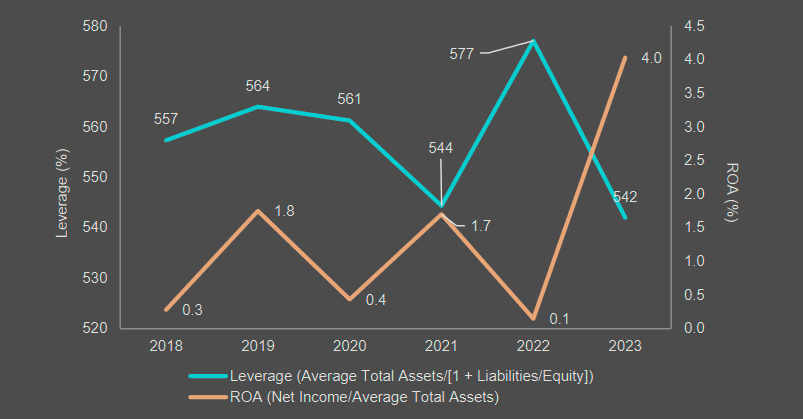

- Reserve leverage for the composite dropped, led by non-life reinsurers, other than the Big Four, which have life as a significant line of business and whose reserve leverage was relatively stable.

The fall in reserve leverage was offset by a significant increase in operating margins. Consequently, the composite’s ROE surpassed its cost of equity after the number of years of falling short, helped additionally by lower taxes and proportionally lower interest on debt.

Global reinsurance market delivered strong results

Global reinsurance market delivered strong results in the first half of 2024 with further improvement in underwriting profitability, exceptional ROEs and a continued building of capital. Earnings resilience has further increased through a higher underlying ROE which provides reinsurers with additional buffer to absorb headwinds.

FY data for global reinsurers indicates that net claims losses of around $15 bn would be necessary for the composite’s ROE to match a cost of capital exceeding 15%, excluding tax implications. AM Best views the hurricane losses as an earnings event rather than a capital one.

While fourth-quarter 2024 results may decline, full-year earnings should remain strong. Reinsurance market conditions are expected to stay stable, as Milton and Helene may delay any softening.

AM Best highlights the complexity of settling claims, including extensive flood losses and tornado activity. The affected regions faced compounded challenges from both hurricanes, testing the terms and conditions of reinsurance contracts. ROEs should be evaluated against the forward-looking cost of capital, such as the Market-Derived Capital Pricing Model (MCPM) (see Global Reinsurance Capital & Catastrophe Bond Market )

AM Best anticipates ROEs will continue exceeding the cost of capital, driven by new capital inflows into established firms and insurance-linked securities markets.

Natural Catastrophe Events Were Frequent, but Reinsurers Adjusted Policies

Secondary natural catastrophe events were frequent, but reinsurers adjusted policies, shifting away from lower layers close to primary perils. The result was the lowest combined and operating ratios seen in five years.

Hurricanes Milton and Helene together could lead to insured losses of $25 bn to $50 bn. A substantial portion of these losses will likely transfer to the global reinsurance market.

However, stricter reinsurance terms and conditions, which led to higher attachment points, also should help make reinsurers’ losses manageable.

Reinsurers are likely to push for double-digit increases in U.S. casualty premium rates during the January 2025 reinsurance renewals. This move aims to address higher loss costs. Rising social inflation in the U.S. casualty sector remains a major risk, keeping the global reinsurance sector outlook neutral.

Analysts expect loss costs to continue rising in 2025 due to social inflation and U.S. legal system abuse. More frequent verdicts that exceed payouts of $10 mn, a higher proportion of claims with attorney involvement, and evolution of the litigation funding industry will add to the trend.

Latent liability risks from opioids, microplastics and synthetic chemical substances known as PFAS pose considerable challenges and uncertainty for casualty reinsurers, according to Fitch Ratings.

Reinsurance Leverage and Investment Shifts

Leverage among reinsurers declined, yet it remains highest at the largest four firms. The composite’s return on assets, boosted by strong underwriting and investment performance, outweighed a slight dip in loss reserve leverage (see about Reinsurer Revenue & Capital Growth ).

AM Best predicts no significant changes in loss reserve leverage and expects continued operating profitability. Investment income should stay strong, even as unrealized capital gains diminish.

Net margins rose sharply in 2024, mainly due to underwriting and investment gains, supported by Bermuda-based deferred tax assets. Asset turnover increased, reflecting higher earned premiums from ongoing rate hikes. AM Best foresees a favorable risk-adjusted market, given current pricing and contract terms.

Global Reinsurance Top 25 Composite – ROE

Source: AM Best data and research

Revenue growth remained strong in 2024 at 9%, similar to the 2023 growth rate. Growth was driven primarily by rate increases rather than volume growth. Volume growth was limited due to shifts in business mix and rising attachment points.

The combined ratio dropped to 84.5%, marking a record low since 2014. This occurred despite a 0.7 percentage point (ppt) decrease in reserve releases and a 0.6 ppt rise in the expense ratio.

The improvement was primarily due to a reduction in the attritional loss ratio (from 68.8% to 66.5%), reflecting rate earn-through and less reserve prudence from some firms, alongside a lower impact from natural catastrophe losses (from 6.8% to 5.6%).

Reinsurers’ Investment Strategies and Tax Impact

Investment returns contributed significantly to net margin growth. While underwriting income was crucial, tax benefits from Bermuda deferred tax assets also played a role. Despite adjustments in investment allocations, reinsurers focused on optimizing for higher returns in a stable interest rate environment.

Investment allocations shifted towards more stable assets. Over six years, the Top 25 reinsurers reduced exposure to private equity and hedge funds, reallocating primarily to US government and corporate bonds. The move, driven by rising interest rates in 2022, brought steadier investment income in 2023-2024.

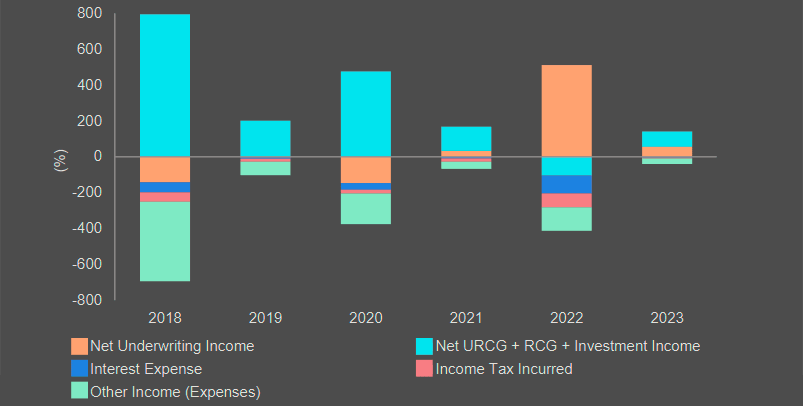

Global Reinsurance Top 25 Composite – Net Income Components

Source: AM Best data and research

This shift toward liquidity and high credit quality investments has strengthened balance sheets and should support financial performance in the short to medium term.

Comments